Research on the Impact of Tax Incentives on Corporate Greenwashing Behavior: Quasi-natural Experiment Based on Value-Added Tax Refund Policy for Input Tax Credits

-

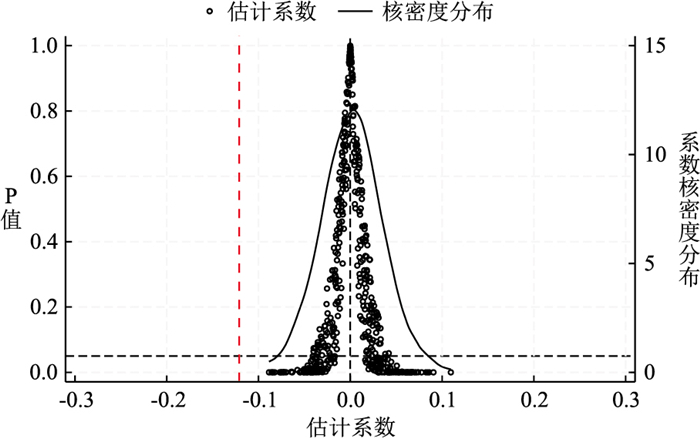

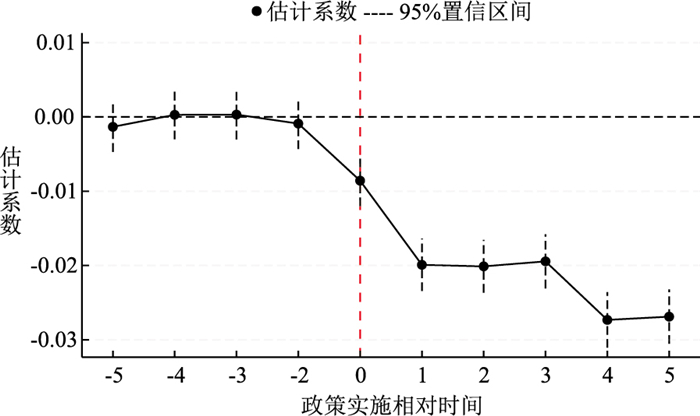

摘要: 我国长期依托税收激励工具引导企业开展绿色转型,增值税留抵退税政策成为财税调控体系中重要的政策抓手。以沪深A股上市公司为研究样本,将2018—2023年留抵退税政策渐进式落地作为多期外生冲击,运用多期双重差分模型展开实证分析。研究发现,留抵退税政策对企业漂绿行为具有显著的抑制作用,其内在作用逻辑体现为双重渠道:一方面,留抵退税通过返还进项税额缓解融资约束,降低企业借助漂绿谋求外部资源的意愿;另一方面,留抵退税依托退税审核流程强化监管效力,压缩企业实施漂绿的操作空间。异质性检验表明,留抵退税抑制效果在环保投入偏低、留抵退税强度较高、基期漂绿水平较高的企业表现得更为显著。本文丰富了税收激励与环境治理交叉领域的研究视角,为优化绿色税收政策、约束企业漂绿行为提供了经验证据。Abstract: China has long relied on tax incentive tools to guide enterprises in green transformation, and the value-added tax (VAT) refund policy for excess input tax credits has become an important policy instrument in the fiscal and taxation regulatory system. Taking A-share listed companies in Shanghai and Shenzhen as research samples, this paper treats the gradual implementation of the VAT refund policy from 2018 to 2023 as a multi-period exogenous shock, and conducts an empirical test using the multi-period difference-in-differences model. The results show that the VAT refund policy significantly inhibits corporate greenwashing behavior through dual channels: on the one hand, the policy eases financing constraints by refunding input tax credits, thereby reducing enterprises' willingness to seek external resources through greenwashing; on the other hand, the policy strengthens regulatory effectiveness through the tax refund review process, compressing the operational space for corporate greenwashing. Heterogeneity tests indicate that the inhibitory effect is more pronounced in enterprises with low environmental investment, high VAT refund intensity, and high baseline greenwashing levels. This paper enriches the research perspective for the intersection of tax incentives and environmental governance, and provides empirical evidence for optimizing green tax policies and restraining corporate greenwashing behavior.

-

Key words:

- tax incentives /

- value-added tax /

- input tax refund /

- corporate greenwashing

-

表 1 主要变量描述性统计结果

变量 样本量 平均值 最大值 标准差 最小值 P25 P75 Greenwash 9 240 -0.141 3.187 1.342 -3.761 -0.985 0.672 Treat_Post 9 240 0.299 1.000 0.458 0 0 1.000 Size 9 240 23.672 27.158 1.384 20.725 22.689 24.513 Lev 9 240 0.479 0.875 0.189 0.080 0.333 0.622 CashFlow 9 240 0.064 0.251 0.065 -0.117 0.024 0.104 SOE 9 240 0.552 1.000 0.497 0 0 1.000 ROA 9 240 0.042 0.189 0.053 -0.215 0.013 0.071 Tangibility 9 240 0.286 0.763 0.162 0.021 0.154 0.408 Dual 9 240 0.205 1.000 0.404 0 0 0 Mshare 9 240 0.063 0.637 0.138 0 0 0.029 SA_abs 9 240 6.195 10.487 1.628 1.938 5.032 7.196 KZ 9 240 1.215 5.892 1.536 -2.107 0.308 2.014 CashRatio 9 240 0.024 0.898 0.154 -0.753 -0.054 0.103 Supervise 9 240 0.186 1.000 0.389 0 0 1.000  下载: 导出CSV

下载: 导出CSV

表 2 基准回归结果

变量 Greenwash

(1)Greenwash

(2)Greenwash

(3)Treat_Post -0.075* -0.121*** (0.040) (0.039) Tax_refund -0.248*** (0.053) Size 0.135*** 0.130*** (0.016) (0.017) Lev -0.512*** -0.508*** (0.091) (0.093) CashFlow 0.473** 0.469** (0.221) (0.223) SOE -0.091*** -0.087*** (0.034) (0.035) Dual 0.132*** 0.129*** (0.038) (0.039) Mshare 0.547*** 0.539*** (0.115) (0.117) ROA -0.326** -0.318** (0.153) (0.155) Tangibility -0.187* -0.182* (0.102) (0.103) Growth -0.058 -0.055 (0.041) (0.042) BoardSize -0.089** -0.085** (0.041) (0.042) IndepRatio -0.215*** -0.208*** (0.067) (0.068) 常数项 -0.403*** -3.487*** -3.426*** (0.019) (0.326) (0.331) 年份固定 是 是 是 个体固定 是 是 是 样本量 9 240 8 862 8 735 Adj.R2 0.005 0.032 0.034 注: *、**、***分别表示10%、5%和1%的显著性水平, 括号内为聚类到企业层面的稳健标准误。下表同。

下载: 导出CSV

表 3 滞后效应、聚类提升和被解释变量替代回归

变量 滞后效应 聚类提升 被解释变量替代 (1) (2) (3) (4) (5) (6) Treat_Post -0.087** -0.105*** -0.112** -0.112*** -0.136*** -0.109*** (0.043) (0.041) (0.051) (0.037) (0.045) (0.036) 常数项 -0.452*** -3.286*** -3.487*** -3.512*** -0.543*** -0.427*** (0.024) (0.367) (0.532) (0.618) (0.162) (0.154) 控制变量 否 是 是 是 否 是 年份固定 是 是 是 是 是 是 个体固定 是 是 是 是 是 是 样本量 7 635 7 328 8 862 8 862 7 943 8 126 Adj.R2 0.003 0.029 0.031 0.032 0.034 0.030

下载: 导出CSV

表 4 PSM-DID回归

变量 最近邻1∶1匹配 最近邻1∶2匹配 Greenwash Greenwash Treat_Post -0.107** -0.116*** (0.053) (0.044) 常数项 -3.277*** -3.234*** (0.585) (0.484) 控制变量 是 是 年份固定 是 是 个体固定 是 是 样本量 3 712 5 369 Adj.R2 0.020 0.022

下载: 导出CSV

表 5 基于双重机器学习的再检验

变量 随机森林法 神经网络法 套索回归法 梯度提升法 Greenwash Greenwash Greenwash Greenwash Treat_Post -0.119*** -0.108*** -0.122*** -0.117*** (0.028) (0.010) (0.030) (0.027) 常数项 -0.008*** -0.097*** -0.001 -0.002 (0.004) (0.012) (0.025) (0.008) 控制变量一次项 是 是 是 是 控制变量二次项 是 是 是 是 年份固定 是 是 是 是 个体固定 是 是 是 是 样本量 9 240 9 240 9 240 9 240

下载: 导出CSV

表 6 融资约束机制检验

变量 融资约束 SA_abs Greenwash KZ Greenwash CashRatio Greenwash (1) (2) (3) (4) (5) (6) Treat_Post -0.021*** -0.071*** -0.084*** -0.069*** 0.039*** -0.070*** (0.008) (0.026) (0.026) (0.025) (0.016) (0.026) SA_abs 0.038*** (0.009) KZ 0.062*** (0.013) CashRatio -0.045*** (0.020) 常数项 6.532*** -1.756*** 2.865*** -1.612*** -0.184*** -1.598*** (0.065) (0.489) (0.217) (0.492) (0.079) (0.490) 控制变量 是 是 是 是 是 是 年份固定 是 是 是 是 是 是 个体固定 是 是 是 是 是 是 样本量 9 240 9 240 9 240 9 240 9 240 9 240 Adj.R2 0.305 0.047 0.026 0.048 0.083 0.046

下载: 导出CSV

表 7 监管效应机制检验

变量 监管效应 Supervise Greenwash (1) (2) Treat_Post 0.213*** -0.068*** (0.045) (0.025) Supervise -0.094*** (0.024) 常数项 0.328*** -1.602*** (0.087) (0.491) 控制变量 是 是 年份固定 是 是 个体固定 是 是 样本量 9 240 9 240 Adj.R2 0.042 0.048

下载: 导出CSV

表 8 异质性分析回归

变量 低环保投入 高环保投入 高退税强度 低退税强度 高漂绿程度 低漂绿程度 (1) (2) (3) (4) (5) (6) Treat_Post -0.153*** -0.068* -0.187*** -0.059 -0.204*** -0.042 (0.041) (0.037) (0.045) (0.038) (0.049) (0.065) 常数项 -3.186*** -2.842** -3.312*** -3.079*** -3.395*** -2.938*** (0.421) (0.397) (0.612) (0.413) (0.436) (0.401) 控制变量 是 是 是 是 是 是 年份固定 是 是 是 是 是 是 个体固定 是 是 是 是 是 是 样本量 4 712 4 528 3 083 3 082 4 619 4 621 Adj.R2 0.287 0.271 0.293 0.265 0.301 0.258

下载: 导出CSV

-

[1] Zhang D Y, Wang J L, Wang Y Z. Greening through centralization of environmental monitoring?[J]. Energy Economics, 2023, 123: 106753. doi: 10.1016/j.eneco.2023.106753 [2] 陈奉功, 张谊浩. 企业发行绿色债券的经济与环境后果研究[J]. 广东财经大学学报, 2023, 38(3): 38-53. http://xb.gdufe.edu.cn/article/id/14bf1b49-6575-422e-b579-ad62e8ba3ebd [3] 姚海东, 李巍. 数字化转型是否抑制了企业的漂绿行为?[J]. 华侨大学学报(哲学社会科学版), 2024(6): 52-69. [4] 于井远, 赵合云, 朱翠华. 减税激励与企业环境、社会和治理表现——基于增值税留抵退税的准自然实验[J]. 当代财经, 2023(10): 44-57. [5] 张云, 杨振宇. 机构投资者绿色关注与企业"漂绿"行为: 效应、诱因与治理[J]. 财经研究, 2024, 50(11): 95-110. [6] 陈瑶. 环境规制执行互动影响工业绿色转型的空间效应研究[J]. 经济问题, 2024(1): 76-83. [7] 聂海峰, 刘怡. 增值税留抵退税政策的影响与分担机制[J]. 经济研究, 2022, 57(8): 78-97. [8] Pfeffer J, Salancik G R. The external control of organizations: a resource dependence perspective[M]. New York: Harper & Row, 1978. [9] Ross S A. The economic theory of agency: the principal's problem[J]. American Economic Review, 1977, 67(2): 303-308. [10] 陈建宇, 沈娇, 蔡闫东. 关键审计事项披露能否抑制企业"漂绿"行为?——基于A股重污染上市公司的证据[J]. 审计与经济研究, 2025, 40(1): 59-72. [11] 岳树民, 肖春明. 增值税留抵退税能够缓解企业融资约束吗——基于现金-现金流敏感性的实证证据[J]. 财贸经济, 2023, 44(1): 51-67. [12] 周文潇, 高婧珂, 杨海霞. 增值税留抵退税政策对企业供应链配置的影响[J]. 经济与管理, 2025, 39(4): 12-20. [13] 鞠晓生, 卢荻, 虞义华. 融资约束、营运资本管理与企业创新可持续性[J]. 经济研究, 2013(1): 4-16. [14] 杨有德, 徐光华, 费锦华. 环境税能否抑制企业"漂绿"行为?[J]. 中国软科学, 2024(5): 132-141. [15] 唐久芳, 李鹏飞, 林晓华. 社会责任报告与环境绩效信息披露的实证研究——来自中国证券市场化工行业的经验数据[J]. 宏观经济研究, 2012(1): 67-72. [16] Zhang D Y. Does green finance really inhibit extreme hypocritical ESG risk? a green washing perspective exploration[J]. Energy Economics, 2023b, 121: 106688. doi: 10.1016/j.eneco.2023.106688 [17] Hadlock C J, Pierce J R. New evidence on measuring financial constraints: moving beyond the KZ Index[J]. Review of Financial Studies, 2010, 23(5): 1909-1940. doi: 10.1093/rfs/hhq009 [18] Kaplan S N, Zingales L. Do investment-cash flow sensitivities provide useful measures of financing constraints?[J]. Quarterly Journal of Economics, 1997, 112(1): 169-215. doi: 10.1162/003355397555163 [19] 徐浩庆, 林浩锋, 邢洁. 环境规制与重污染企业的ESG表现[J]. 广东财经大学学报, 2024, 39(1): 85-99. http://xb.gdufe.edu.cn/article/id/8ac7686f-cf03-4c5d-8dfb-7cd49e360e45 [20] 马亚明, 徐会杰, 王一婕. 董事高管责任保险与企业ESG表现[J]. 广东财经大学学报, 2024, 39(4): 70-84. http://xb.gdufe.edu.cn/article/id/ac3b52ed-0557-4596-847a-a573192d7e9d [21] 徐斯旸, 丁子家, 向海凌, 等. "金融科技-实体经济"匹配与企业绿色转型[J]. 财贸经济, 2024, 45(11): 56-72. [22] 李玉姣, 李骥骁, 辛冲冲. 增值税留抵退税对企业绿色创新的影响研究[J]. 财经论丛, 2025, 41(1): 26-36. [23] 崔小勇, 蔡昀珊, 卢国军. 增值税留抵退税能否促进企业吸纳就业?——来自2019年试行留抵退税制度的证据[J]. 管理世界, 2023, 39(9): 15-35. [24] 吴烨伟, 郝若鸿, 韩宇航. 增值税留抵退税的环境治理效应: 绿色并购的视角[J]. 管理科学, 2023, 36(5): 18-31. [25] 张凯. 数字税收征管能提升企业创新能力吗?——基于研发操纵和盈余管理的中介效应[J]. 河北经贸大学学报, 2025, 46(2): 88-98. [26] 刘同洲, 李万甫. 基于数据增值的税收征管数字化转型路径研究[J]. 财政研究, 2022(4): 119-129. -

点击查看大图

点击查看大图

图(2) / 表(8)

计量

- 文章访问数: 794

- HTML全文浏览量: 1298

- PDF下载量: 32

- 被引次数: 0