Submission System

Submission Guidelines

Articles in press have been peer-reviewed and accepted, which are not yet assigned to volumes /issues, but are citable by Digital Object Identifier (DOI).

Display Method:

Display Method:

2026, 41(3): 4-16.

Abstract:

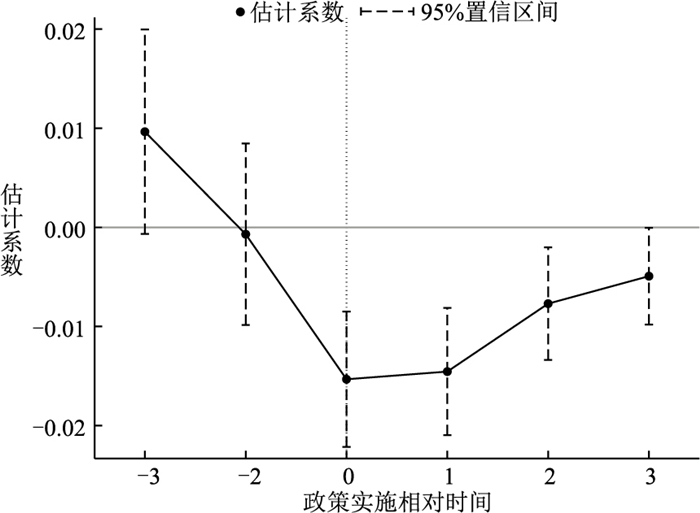

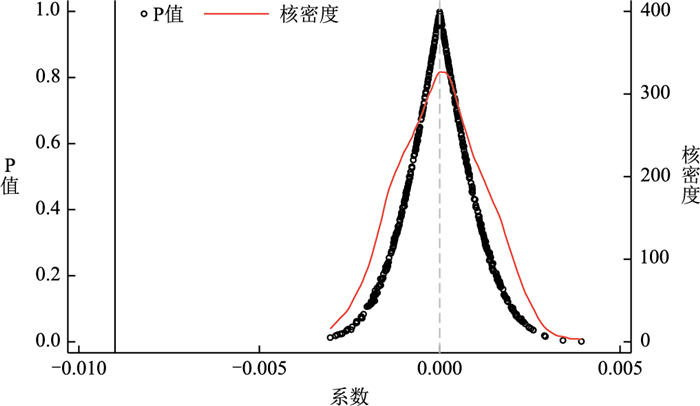

Against the backdrop of the accelerated evolution of digital technologies intertwined with external shocks from global uncertainties, the vigorous development of artificial intelligence has become a core way to drive technological innovation and strengthen the resilience of China's economy. Based on the sample of Shanghai and Shenzhen A-share listed firms from 2010 to 2023, this paper explores the influence of artificial intelligence on corporate organizational resilience as well as its internal mechanism. The empirical results reveal that the application of artificial intelligence can significantly boost the level of enterprise organizational resilience. Mechanism tests further indicate that artificial intelligence can realize the systematic improvement of organizational resilience through three multidimensional paths, namely decision empowerment, operational empowerment and innovation empowerment. Heterogeneity analysis shows that such promotional effect is more pronounced among technology-intensive enterprises, small and medium-sized firms, non-state-owned enterprises, and enterprises operating in competitive industries. Further research also indicates that artificial intelligence could generate resilience spillover effects on upstream and downstream enterprises via supply chain linkages. Meanwhile, the improvement of individual organizational resilience can greatly enhance the overall resilience of the whole supply chain. Accordingly, relevant policies on artificial intelligence development should be steadily advanced in the future, so as to give full play to the amplification, superposition and multiplication effects of digital technology and fully release the development dividends brought by artificial intelligence.

Against the backdrop of the accelerated evolution of digital technologies intertwined with external shocks from global uncertainties, the vigorous development of artificial intelligence has become a core way to drive technological innovation and strengthen the resilience of China's economy. Based on the sample of Shanghai and Shenzhen A-share listed firms from 2010 to 2023, this paper explores the influence of artificial intelligence on corporate organizational resilience as well as its internal mechanism. The empirical results reveal that the application of artificial intelligence can significantly boost the level of enterprise organizational resilience. Mechanism tests further indicate that artificial intelligence can realize the systematic improvement of organizational resilience through three multidimensional paths, namely decision empowerment, operational empowerment and innovation empowerment. Heterogeneity analysis shows that such promotional effect is more pronounced among technology-intensive enterprises, small and medium-sized firms, non-state-owned enterprises, and enterprises operating in competitive industries. Further research also indicates that artificial intelligence could generate resilience spillover effects on upstream and downstream enterprises via supply chain linkages. Meanwhile, the improvement of individual organizational resilience can greatly enhance the overall resilience of the whole supply chain. Accordingly, relevant policies on artificial intelligence development should be steadily advanced in the future, so as to give full play to the amplification, superposition and multiplication effects of digital technology and fully release the development dividends brought by artificial intelligence.

2026, 41(3): 17-32.

Abstract:

With the profound advancement of artificial intelligence technology, computing power resources are gradually replacing traditional production factors as the key driver for enhancing corporate resilience. Given that intelligent computing centers serve as the core physical infrastructure for computing power deployment, this study examines whether and how such centers influence the resilience of upstream and downstream enterprises. The research reveals that the computing power deployment by central enterprises significantly enhances the resilience of their supply chain partners. Mechanism analysis demonstrates that for upstream suppliers, central enterprises strengthen resilience through three primary channels: optimizing resource allocation, providing supply chain financing support, and promoting supply chain decentralization; for downstream clients, resilience improvement is achieved via three mechanisms: increasing supply chain transparency, enhancing agile responsiveness, and boosting innovation capabilities. Further analysis reveals significant spatial distribution and structural variations in these effects. This study expands the theoretical framework of digital infrastructure research from a computing power perspective, offering policy insights to foster high-quality corporate development and strengthen the foundation of the digital economy.

With the profound advancement of artificial intelligence technology, computing power resources are gradually replacing traditional production factors as the key driver for enhancing corporate resilience. Given that intelligent computing centers serve as the core physical infrastructure for computing power deployment, this study examines whether and how such centers influence the resilience of upstream and downstream enterprises. The research reveals that the computing power deployment by central enterprises significantly enhances the resilience of their supply chain partners. Mechanism analysis demonstrates that for upstream suppliers, central enterprises strengthen resilience through three primary channels: optimizing resource allocation, providing supply chain financing support, and promoting supply chain decentralization; for downstream clients, resilience improvement is achieved via three mechanisms: increasing supply chain transparency, enhancing agile responsiveness, and boosting innovation capabilities. Further analysis reveals significant spatial distribution and structural variations in these effects. This study expands the theoretical framework of digital infrastructure research from a computing power perspective, offering policy insights to foster high-quality corporate development and strengthen the foundation of the digital economy.

2026, 41(3): 33-48.

Abstract:

Driven by the strategy of building a trading power and amid the profound restructuring of the global trade landscape, digital technology application has become a core path for China to break through traditional competitive barriers and build new advantages in international competition. Taking 285 prefecture-level cities from 2009 to 2023 as the research sample, this paper deeply explores the effect and mechanism of digital technology application on urban export resilience. The study finds that digital technology application significantly enhances urban export resilience, and this conclusion has passed a series of robustness tests and endogeneity tests. Mechanism tests reveal that digital technology application can empower urban export resilience by alleviating resource misallocation and improving innovation efficiency. Moderating effect analysis shows that both the "proactive government" and the "efficient market" can strengthen the impact of digital technology application on urban export resilience. Heterogeneity analysis indicates that the empowering effect of digital technology application is more prominent in regions southeast of the Hu Huanyong Line, regions with higher initial levels of digital infrastructure, and regions with stronger intellectual property protection. This study provides important theoretical support and empirical evidence for unlocking the value of digital technology application and enhancing urban export resilience.

Driven by the strategy of building a trading power and amid the profound restructuring of the global trade landscape, digital technology application has become a core path for China to break through traditional competitive barriers and build new advantages in international competition. Taking 285 prefecture-level cities from 2009 to 2023 as the research sample, this paper deeply explores the effect and mechanism of digital technology application on urban export resilience. The study finds that digital technology application significantly enhances urban export resilience, and this conclusion has passed a series of robustness tests and endogeneity tests. Mechanism tests reveal that digital technology application can empower urban export resilience by alleviating resource misallocation and improving innovation efficiency. Moderating effect analysis shows that both the "proactive government" and the "efficient market" can strengthen the impact of digital technology application on urban export resilience. Heterogeneity analysis indicates that the empowering effect of digital technology application is more prominent in regions southeast of the Hu Huanyong Line, regions with higher initial levels of digital infrastructure, and regions with stronger intellectual property protection. This study provides important theoretical support and empirical evidence for unlocking the value of digital technology application and enhancing urban export resilience.

2026, 41(3): 49-64.

Abstract:

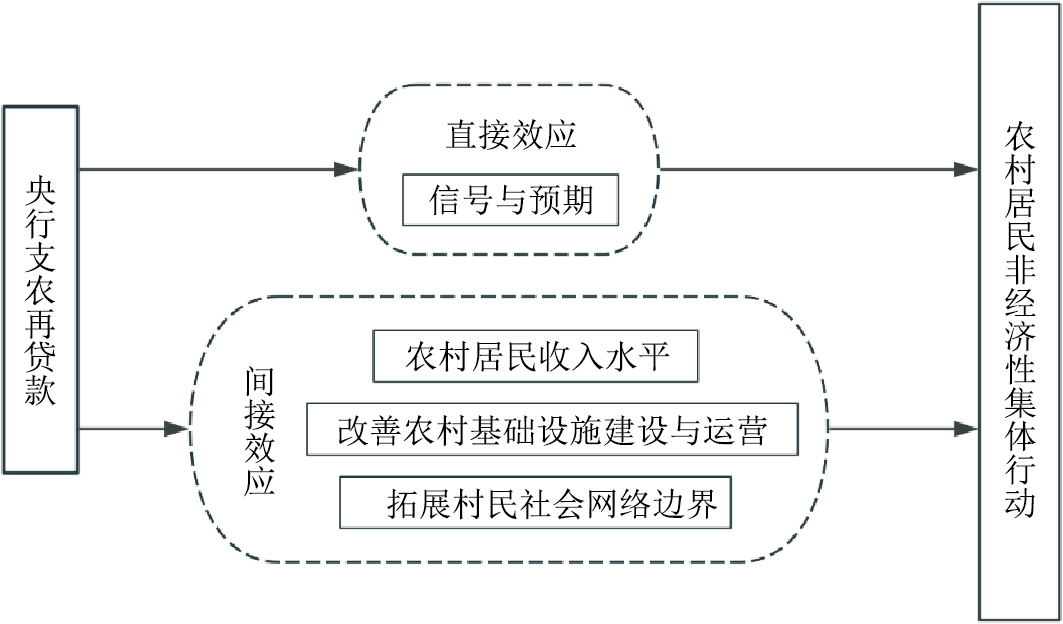

The non-economic collective action of rural residents constitutes an indispensable component of rural public affairs governance and rural residents' spontaneous operations, and serves as a vital pathway toward comprehensive rural revitalization. Drawing on micro data from the China Labor-force Dynamics Survey (CLDS) and employing a panel fixed-effect model, this paper empirically investigates the effects and mechanisms of agricultural support relending. The findings reveal that agricultural support relending not only positively promotes the overall non-economic collective action of rural residents, but also exhibits varying degrees of facilitating effects on different types of collective action. Mechanism tests demonstrate that agricultural support relending plays a mediating role in fostering rural residents' non-economic collective action through three channels: raising rural residents' income levels, improving the construction and operation of rural infrastructure, and expanding the boundaries of villagers' social networks. Heterogeneity analysis indicates that the promoting effect of agricultural support relending on collective action is more pronounced among credit beneficiary groups and collective fund-raising participants, as well as in large villages and villages with moderate economic development. This paper provides micro-level evidence on the impact of agricultural support relending on rural residents' non-economic collective action, aiming to uncover the specific pathways through which financial instruments, by alleviating economic constraints, induce the accumulation of social capital and improvements in social governance. It thereby supplies a theoretical foundation and policy references for strengthening rural governance and advancing comprehensive rural revitalization.

The non-economic collective action of rural residents constitutes an indispensable component of rural public affairs governance and rural residents' spontaneous operations, and serves as a vital pathway toward comprehensive rural revitalization. Drawing on micro data from the China Labor-force Dynamics Survey (CLDS) and employing a panel fixed-effect model, this paper empirically investigates the effects and mechanisms of agricultural support relending. The findings reveal that agricultural support relending not only positively promotes the overall non-economic collective action of rural residents, but also exhibits varying degrees of facilitating effects on different types of collective action. Mechanism tests demonstrate that agricultural support relending plays a mediating role in fostering rural residents' non-economic collective action through three channels: raising rural residents' income levels, improving the construction and operation of rural infrastructure, and expanding the boundaries of villagers' social networks. Heterogeneity analysis indicates that the promoting effect of agricultural support relending on collective action is more pronounced among credit beneficiary groups and collective fund-raising participants, as well as in large villages and villages with moderate economic development. This paper provides micro-level evidence on the impact of agricultural support relending on rural residents' non-economic collective action, aiming to uncover the specific pathways through which financial instruments, by alleviating economic constraints, induce the accumulation of social capital and improvements in social governance. It thereby supplies a theoretical foundation and policy references for strengthening rural governance and advancing comprehensive rural revitalization.

2026, 41(3): 65-78.

Abstract:

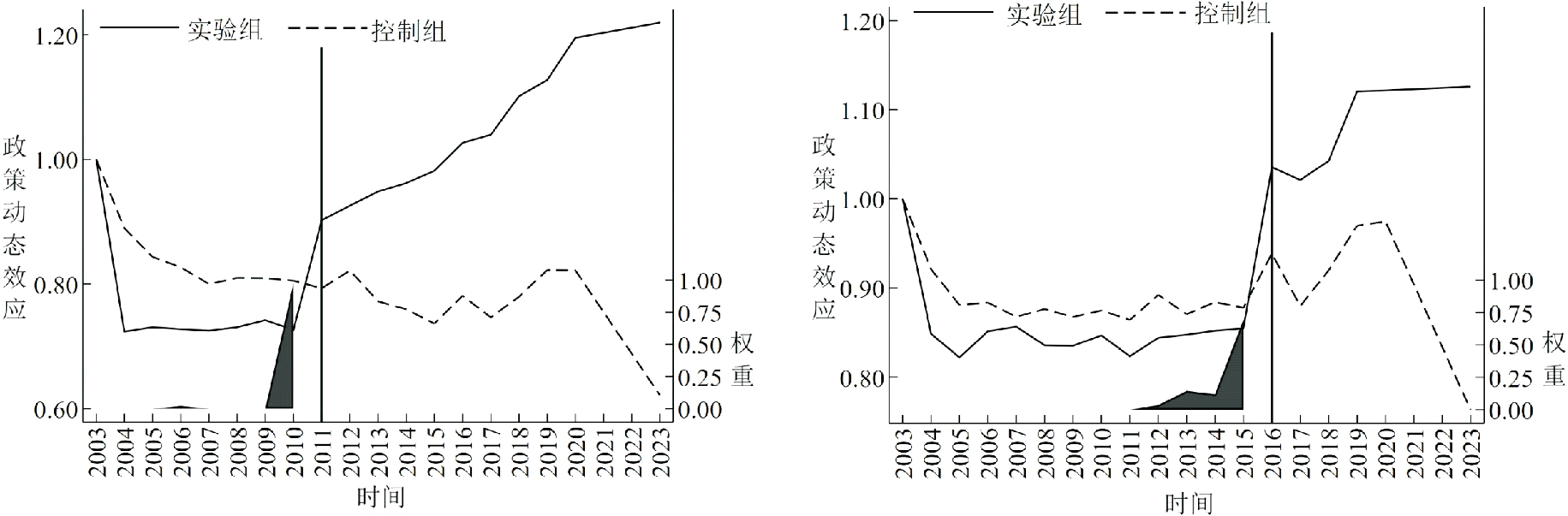

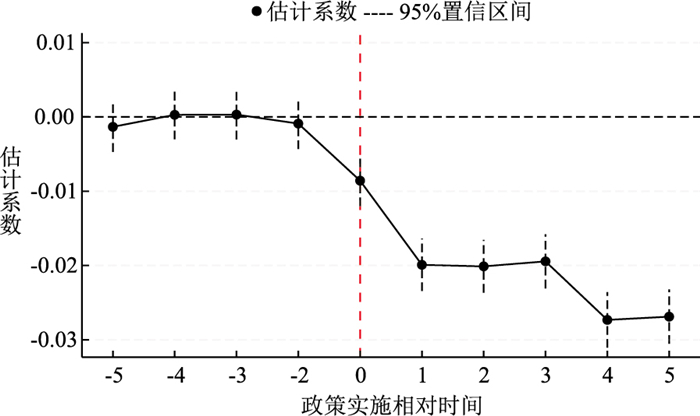

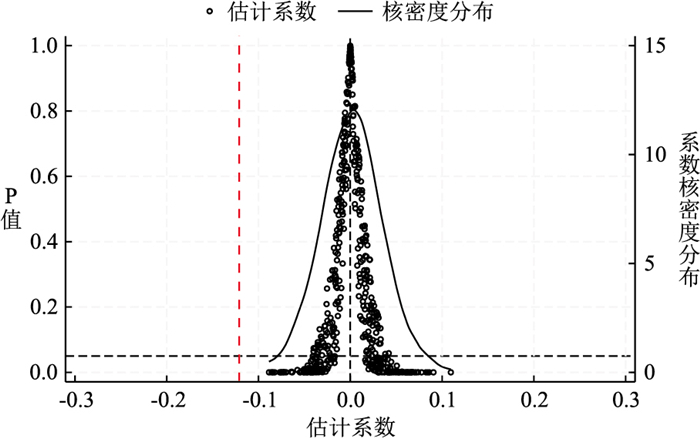

As the core engine for realizing green and sustainable development, low-carbon economic transition depends on in-depth empowerment of sci-tech innovation and efficient allocation of financial resources. Using panel data from 281 prefecture-level and above cities in China from 2003 to 2023, this paper employs a synthetic control method with difference-in-differences (SDID) to integrate the low-carbon economic transition into the evaluation framework of the sci-tech financial policy, and empirically analyzes its impact on low-carbon economic transition combined with the three-dimensional linkage mechanism of industries, enterprises and researchers. The results reveal that the sci-tech financial policy exert a significant promoting effect on low-carbon economic transition, with industrial chain resilience, artificial intelligence development level and sci-tech innovation vitality serving as core influencing mechanisms. Its impact on low-carbon economic transition of surrounding cities presents fluctuating spatial transmission characteristics. The role of sci-tech financial policy is more significant in cities with net population inflow, non-old industrial base cities, and coastal cities. The research findings provide practical references and policy insights for optimizing the allocation of sci-tech finance resources, enhancing the efficiency of low-carbon economic transition, and promoting regional green coordinated development.

As the core engine for realizing green and sustainable development, low-carbon economic transition depends on in-depth empowerment of sci-tech innovation and efficient allocation of financial resources. Using panel data from 281 prefecture-level and above cities in China from 2003 to 2023, this paper employs a synthetic control method with difference-in-differences (SDID) to integrate the low-carbon economic transition into the evaluation framework of the sci-tech financial policy, and empirically analyzes its impact on low-carbon economic transition combined with the three-dimensional linkage mechanism of industries, enterprises and researchers. The results reveal that the sci-tech financial policy exert a significant promoting effect on low-carbon economic transition, with industrial chain resilience, artificial intelligence development level and sci-tech innovation vitality serving as core influencing mechanisms. Its impact on low-carbon economic transition of surrounding cities presents fluctuating spatial transmission characteristics. The role of sci-tech financial policy is more significant in cities with net population inflow, non-old industrial base cities, and coastal cities. The research findings provide practical references and policy insights for optimizing the allocation of sci-tech finance resources, enhancing the efficiency of low-carbon economic transition, and promoting regional green coordinated development.

2026, 41(3): 79-90.

Abstract:

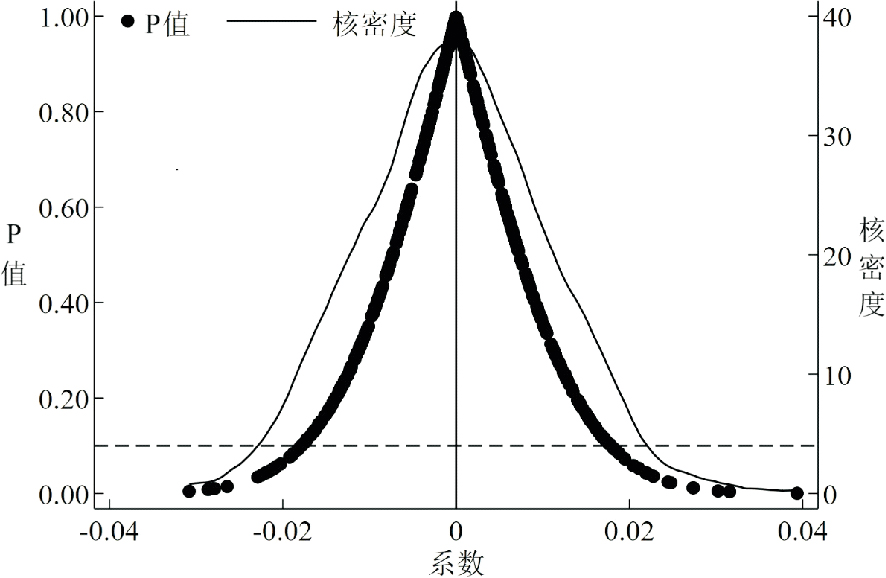

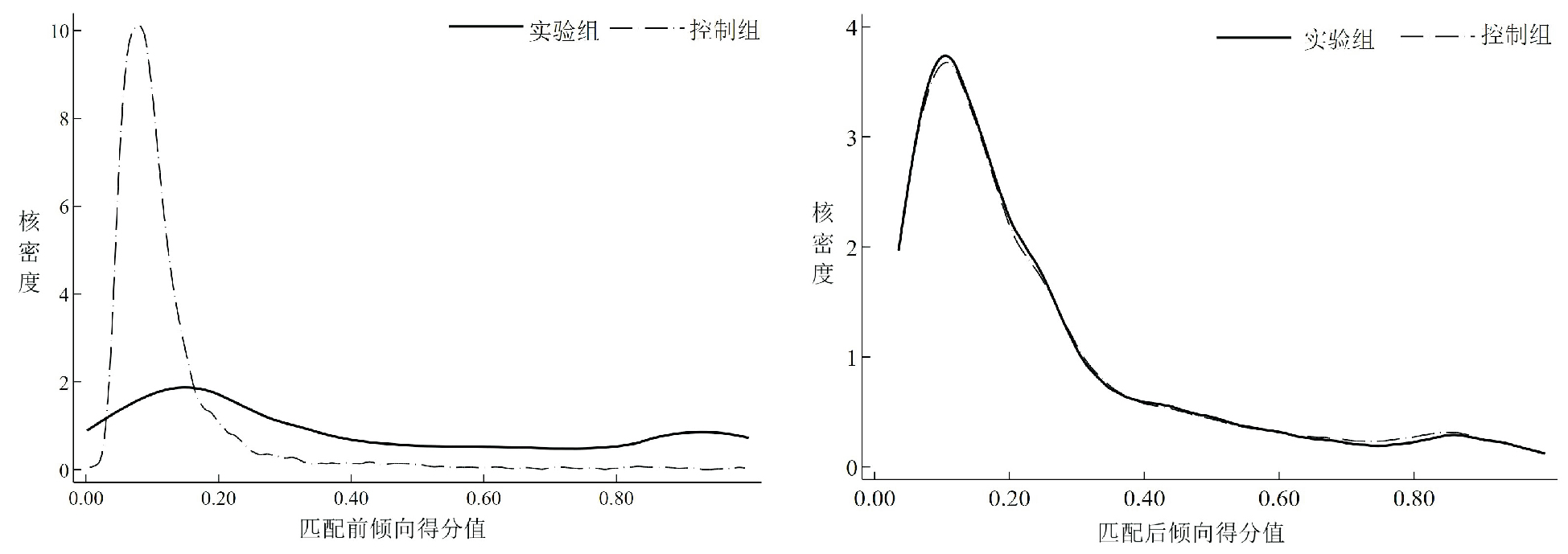

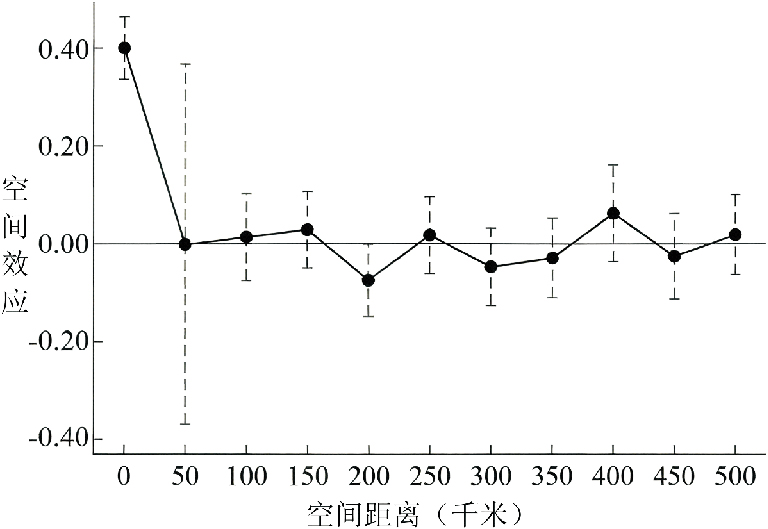

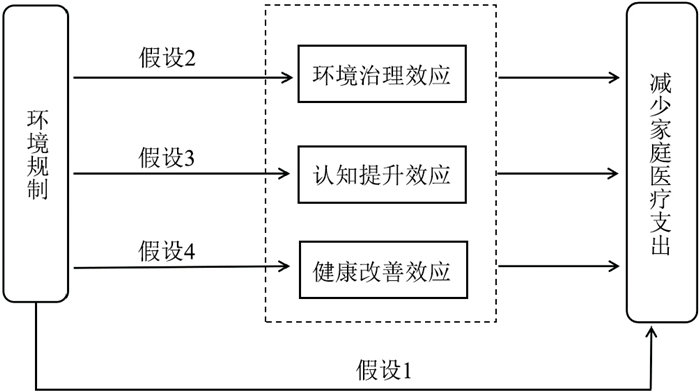

Against the strategic backdrop of the coordinated advancement of the Beautiful China Initiative and Healthy China Initiative, exploring the impact of environmental regulation on household medical expenditure is of great theoretical and practical significance. Based on China's prefecture-level city data from 2013 to 2020 and micro data from four waves of the China Health and Retirement Longitudinal Study (CHARLS), this paper empirically examines the impact of environmental regulation on medical expenditure of middle-aged and elderly households. The results show that environmental regulation significantly reduces medical expenditure of middle-aged and elderly households. This core conclusion still holds after endogeneity treatment and a series of robustness tests. Mechanism analysis reveals that environmental regulation curbs medical expenditure of middle-aged and elderly households through three pathways: environmental governance, health cognition improvement, and health improvement. Heterogeneity analysis shows that, at the household level, environmental regulation has a stronger inhibitory effect on medical expenditure of middle-aged and low-income households. At the regional level, households in resource-based cities and non-key environmental protection cities exhibit greater sensitivity to environmental regulation in terms of health spending. From the micro household perspective, this study expands the research scope of environmental regulation's influence on health expenditure, and provides empirical evidence for coordinating ecological civilization construction and national health development.

Against the strategic backdrop of the coordinated advancement of the Beautiful China Initiative and Healthy China Initiative, exploring the impact of environmental regulation on household medical expenditure is of great theoretical and practical significance. Based on China's prefecture-level city data from 2013 to 2020 and micro data from four waves of the China Health and Retirement Longitudinal Study (CHARLS), this paper empirically examines the impact of environmental regulation on medical expenditure of middle-aged and elderly households. The results show that environmental regulation significantly reduces medical expenditure of middle-aged and elderly households. This core conclusion still holds after endogeneity treatment and a series of robustness tests. Mechanism analysis reveals that environmental regulation curbs medical expenditure of middle-aged and elderly households through three pathways: environmental governance, health cognition improvement, and health improvement. Heterogeneity analysis shows that, at the household level, environmental regulation has a stronger inhibitory effect on medical expenditure of middle-aged and low-income households. At the regional level, households in resource-based cities and non-key environmental protection cities exhibit greater sensitivity to environmental regulation in terms of health spending. From the micro household perspective, this study expands the research scope of environmental regulation's influence on health expenditure, and provides empirical evidence for coordinating ecological civilization construction and national health development.

2026, 41(3): 91-104.

Abstract:

ESG rating divergence is a key source of cognitive bias in capital markets' assessment of corporate ESG performance. Using Chinese A-share listed firms from 2013 to 2023 as the research sample and exploiting the pilot reform of the social credit system as a quasi-natural experiment, this paper examines the impact of social credit improvement on corporate ESG rating divergence and its underlying mechanisms. The results show that social credit improvement significantly reduces ESG rating divergence. Mechanism tests indicate that social credit improvement operates through both an "information effect"and a "governance effect": it alleviates information asymmetry and reduces rating agencies' reliance on private information, while also improving internal control quality and curbing greenwashing risk, thereby lowering ESG rating divergence. Heterogeneity analysis shows that the mitigating effect of improved social credit on ESG rating disagreement is mainly reflected in the governance (G) dimension, and is more pronounced among firms located in regions with stronger environmental regulation and greater public environmental attention, as well as among heavily polluting firms and firms whose management teams lack environmental backgrounds. Economic consequence analysis shows that by reducing ESG rating divergence, social credit improvement helps lower stock price crash risk and supply chain risk, thereby enhancing firms' stability in both capital and product markets. This study extends the literature on the positive effects of social credit system development and provides implications for improving the ESG governance system and promoting high-quality sustainable development.

ESG rating divergence is a key source of cognitive bias in capital markets' assessment of corporate ESG performance. Using Chinese A-share listed firms from 2013 to 2023 as the research sample and exploiting the pilot reform of the social credit system as a quasi-natural experiment, this paper examines the impact of social credit improvement on corporate ESG rating divergence and its underlying mechanisms. The results show that social credit improvement significantly reduces ESG rating divergence. Mechanism tests indicate that social credit improvement operates through both an "information effect"and a "governance effect": it alleviates information asymmetry and reduces rating agencies' reliance on private information, while also improving internal control quality and curbing greenwashing risk, thereby lowering ESG rating divergence. Heterogeneity analysis shows that the mitigating effect of improved social credit on ESG rating disagreement is mainly reflected in the governance (G) dimension, and is more pronounced among firms located in regions with stronger environmental regulation and greater public environmental attention, as well as among heavily polluting firms and firms whose management teams lack environmental backgrounds. Economic consequence analysis shows that by reducing ESG rating divergence, social credit improvement helps lower stock price crash risk and supply chain risk, thereby enhancing firms' stability in both capital and product markets. This study extends the literature on the positive effects of social credit system development and provides implications for improving the ESG governance system and promoting high-quality sustainable development.

2026, 41(3): 105-116.

Abstract:

Presetting annual employment growth targets is a key measure for Chinese governments at all levels to stabilize employment, yet this practice tends to distort resource allocation and cause productivity losses. Based on the employment growth targets specified in the government work reports of prefecture-level cities from 2014 to 2024, combined with data on A-share listed companies, this paper examines the impact of local employment targets on enterprises' total factor productivity (TFP). The results show that the employment growth target system significantly inhibits enterprises' TFP. Specifically, for every 10% increase in the local employment growth target, the enterprise TFP decreases by 0.16%, with a more pronounced effect in state-owned enterprises, labor-intensive industries, and regions with higher target fulfillment rates. Mechanism analysis indicates that local employment targets lower productivity by aggravating labor redundancy and restraining human resource reallocation. From a cost-benefit perspective, although these targets can expand short-term employment, this effect fails to offset the negative impact of productivity losses on operating revenue. Furthermore, the long-term erosion of profit margins weakens enterprises' sustainable employment capacity. This study reveals the productivity loss risk of the employment target system, providing insights for optimizing target setting and achieving policy coordination between stabilizing employment and boosting enterprise productivity.

Presetting annual employment growth targets is a key measure for Chinese governments at all levels to stabilize employment, yet this practice tends to distort resource allocation and cause productivity losses. Based on the employment growth targets specified in the government work reports of prefecture-level cities from 2014 to 2024, combined with data on A-share listed companies, this paper examines the impact of local employment targets on enterprises' total factor productivity (TFP). The results show that the employment growth target system significantly inhibits enterprises' TFP. Specifically, for every 10% increase in the local employment growth target, the enterprise TFP decreases by 0.16%, with a more pronounced effect in state-owned enterprises, labor-intensive industries, and regions with higher target fulfillment rates. Mechanism analysis indicates that local employment targets lower productivity by aggravating labor redundancy and restraining human resource reallocation. From a cost-benefit perspective, although these targets can expand short-term employment, this effect fails to offset the negative impact of productivity losses on operating revenue. Furthermore, the long-term erosion of profit margins weakens enterprises' sustainable employment capacity. This study reveals the productivity loss risk of the employment target system, providing insights for optimizing target setting and achieving policy coordination between stabilizing employment and boosting enterprise productivity.

2026, 41(3): 117-128.

Abstract:

China has long relied on tax incentive tools to guide enterprises in green transformation, and the value-added tax (VAT) refund policy for excess input tax credits has become an important policy instrument in the fiscal and taxation regulatory system. Taking A-share listed companies in Shanghai and Shenzhen as research samples, this paper treats the gradual implementation of the VAT refund policy from 2018 to 2023 as a multi-period exogenous shock, and conducts an empirical test using the multi-period difference-in-differences model. The results show that the VAT refund policy significantly inhibits corporate greenwashing behavior through dual channels: on the one hand, the policy eases financing constraints by refunding input tax credits, thereby reducing enterprises' willingness to seek external resources through greenwashing; on the other hand, the policy strengthens regulatory effectiveness through the tax refund review process, compressing the operational space for corporate greenwashing. Heterogeneity tests indicate that the inhibitory effect is more pronounced in enterprises with low environmental investment, high VAT refund intensity, and high baseline greenwashing levels. This paper enriches the research perspective for the intersection of tax incentives and environmental governance, and provides empirical evidence for optimizing green tax policies and restraining corporate greenwashing behavior.

China has long relied on tax incentive tools to guide enterprises in green transformation, and the value-added tax (VAT) refund policy for excess input tax credits has become an important policy instrument in the fiscal and taxation regulatory system. Taking A-share listed companies in Shanghai and Shenzhen as research samples, this paper treats the gradual implementation of the VAT refund policy from 2018 to 2023 as a multi-period exogenous shock, and conducts an empirical test using the multi-period difference-in-differences model. The results show that the VAT refund policy significantly inhibits corporate greenwashing behavior through dual channels: on the one hand, the policy eases financing constraints by refunding input tax credits, thereby reducing enterprises' willingness to seek external resources through greenwashing; on the other hand, the policy strengthens regulatory effectiveness through the tax refund review process, compressing the operational space for corporate greenwashing. Heterogeneity tests indicate that the inhibitory effect is more pronounced in enterprises with low environmental investment, high VAT refund intensity, and high baseline greenwashing levels. This paper enriches the research perspective for the intersection of tax incentives and environmental governance, and provides empirical evidence for optimizing green tax policies and restraining corporate greenwashing behavior.

2026, 41(3): 129-145.

Abstract:

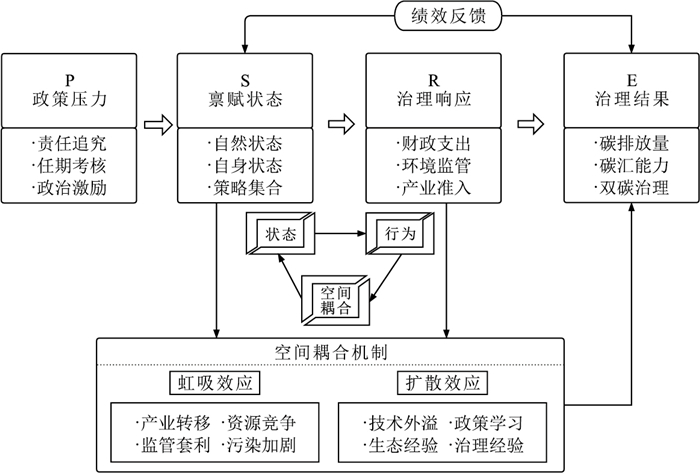

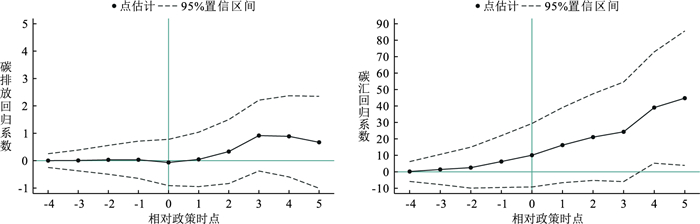

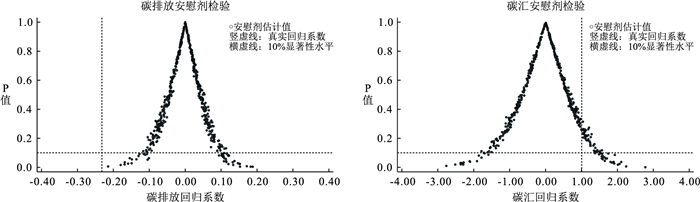

The accountability audit of natural resources (AANR) is a distinct institutional innovation in China that systematically constrains local environmental governance. By integrating ecological responsibility into political incentives, it aims to shift the economic growth away from a GDP-oriented paradigm. Exploiting the staggered pilot rollout of the policy as a quasi-natural experiment, this study matches city-level carbon emissions and carbon sink data for 285 Chinese cities from 2011 to 2020 with audit pilot information. This study employs a multi-period difference-in-differences model (DID) and a spatial Durbin model (SDM) to evaluate its governance effects on the "dual-carbon" targets. The results show that AANR significantly reduces carbon emission intensity and enhances carbon sink capacity, indicating clear direct governance effects. Spatial impacts exhibit dimensional heterogeneity. Geographically proximate regions display diffusion effects driven by technological spillovers, while areas within the same administrative jurisdiction show siphoning effects characterized by pollution transfer. Further analysis finds that when neighboring regions are simultaneously audited, positive spillovers are weakened and may even reverse within provinces, suggesting strategic interactions among local governments under environmental regulation. This study also documents an administrative clustering pattern in carbon emissions, indicating that the dual-carbon transition is largely driven by government intervention. This study provides key evidence on the effectiveness of government-led environmental governance in China. It confirms the institutional value of AANR and offers policy implications for improving regional coordination and advancing integrated governance.

The accountability audit of natural resources (AANR) is a distinct institutional innovation in China that systematically constrains local environmental governance. By integrating ecological responsibility into political incentives, it aims to shift the economic growth away from a GDP-oriented paradigm. Exploiting the staggered pilot rollout of the policy as a quasi-natural experiment, this study matches city-level carbon emissions and carbon sink data for 285 Chinese cities from 2011 to 2020 with audit pilot information. This study employs a multi-period difference-in-differences model (DID) and a spatial Durbin model (SDM) to evaluate its governance effects on the "dual-carbon" targets. The results show that AANR significantly reduces carbon emission intensity and enhances carbon sink capacity, indicating clear direct governance effects. Spatial impacts exhibit dimensional heterogeneity. Geographically proximate regions display diffusion effects driven by technological spillovers, while areas within the same administrative jurisdiction show siphoning effects characterized by pollution transfer. Further analysis finds that when neighboring regions are simultaneously audited, positive spillovers are weakened and may even reverse within provinces, suggesting strategic interactions among local governments under environmental regulation. This study also documents an administrative clustering pattern in carbon emissions, indicating that the dual-carbon transition is largely driven by government intervention. This study provides key evidence on the effectiveness of government-led environmental governance in China. It confirms the institutional value of AANR and offers policy implications for improving regional coordination and advancing integrated governance.

2019, 34(6): 35-49.

摘要:

数字普惠金融发展对产业结构升级具有重要积极意义。在对数字普惠金融发展与产业结构升级之间的关系进行理论分析的基础上, 基于283个地级以上城市2011—2015年的面板数据, 采用面板门槛模型等回归方法, 实证分析数字普惠金融发展及其各维度发展与产业结构升级之间的关系。结果表明: 数字普惠金融发展与产业结构升级之间存在非线性关系; 数字普惠金融发展存在瓶颈, 具有门槛效应; 数字普惠金融覆盖广度对产业结构升级具有长期且显著的促进作用, 数字普惠金融的使用深度和数字化程度与产业结构升级之间存在非线性关系; 不同区域的数字普惠金融发展对产业结构升级的非线性效应具有异质性, 对产业结构升级的正效应从东部到中西部逐级增强。因而政府部门和金融机构应加大建设数字金融基础设施的力度, 尤其要重视增加落后地区的普惠金融服务供给和提升其数字化程度, 同时, 也要防止数字普惠金融的过度发展为产业结构升级带来负的外部效应。

数字普惠金融发展对产业结构升级具有重要积极意义。在对数字普惠金融发展与产业结构升级之间的关系进行理论分析的基础上, 基于283个地级以上城市2011—2015年的面板数据, 采用面板门槛模型等回归方法, 实证分析数字普惠金融发展及其各维度发展与产业结构升级之间的关系。结果表明: 数字普惠金融发展与产业结构升级之间存在非线性关系; 数字普惠金融发展存在瓶颈, 具有门槛效应; 数字普惠金融覆盖广度对产业结构升级具有长期且显著的促进作用, 数字普惠金融的使用深度和数字化程度与产业结构升级之间存在非线性关系; 不同区域的数字普惠金融发展对产业结构升级的非线性效应具有异质性, 对产业结构升级的正效应从东部到中西部逐级增强。因而政府部门和金融机构应加大建设数字金融基础设施的力度, 尤其要重视增加落后地区的普惠金融服务供给和提升其数字化程度, 同时, 也要防止数字普惠金融的过度发展为产业结构升级带来负的外部效应。

2021, 36(5): 27-40.

摘要:

数字经济是经济发展提质增效的新动能和新引擎,对产业结构的转型升级具有重要驱动作用。在理论分析的基础上,从产业转型速度、产业结构高度化以及产业结构合理化三个维度对产业结构的转型升级进行分解,以区域创新创业指数表征城市创新创业水平,采用2011—2018年我国城市面板数据实证考察数字经济发展的产业结构转型升级效应及其作用机制。研究发现:(1)数字经济能显著提升产业转型速度、产业结构高度化和产业结构合理化,且基于互联网发展和数字普惠金融发展的分析结果趋同。(2)数字经济对产业结构转型升级的效应具有边际报酬递增的后发性优势,且东中西部区域异质性特征明显,其中中部地区是未来数字经济发展的重心。(3)从城市规模看,中等城市和大城市是数字经济驱动产业转型升级的重要着力点;从城市等级来看,二三线城市是产业转型的关键所在。(4)中介效应分析显示,创新创业水平是数字经济产业转型升级效应的重要传导路径,数字经济通过激发区域创新创业活力可加快产业转型速度、促进产业结构的高度化和合理化。以上结论对探索中国城市数字经济可持续发展、助推其与产业结构转型升级深度融合具有一定的参考意义。

数字经济是经济发展提质增效的新动能和新引擎,对产业结构的转型升级具有重要驱动作用。在理论分析的基础上,从产业转型速度、产业结构高度化以及产业结构合理化三个维度对产业结构的转型升级进行分解,以区域创新创业指数表征城市创新创业水平,采用2011—2018年我国城市面板数据实证考察数字经济发展的产业结构转型升级效应及其作用机制。研究发现:(1)数字经济能显著提升产业转型速度、产业结构高度化和产业结构合理化,且基于互联网发展和数字普惠金融发展的分析结果趋同。(2)数字经济对产业结构转型升级的效应具有边际报酬递增的后发性优势,且东中西部区域异质性特征明显,其中中部地区是未来数字经济发展的重心。(3)从城市规模看,中等城市和大城市是数字经济驱动产业转型升级的重要着力点;从城市等级来看,二三线城市是产业转型的关键所在。(4)中介效应分析显示,创新创业水平是数字经济产业转型升级效应的重要传导路径,数字经济通过激发区域创新创业活力可加快产业转型速度、促进产业结构的高度化和合理化。以上结论对探索中国城市数字经济可持续发展、助推其与产业结构转型升级深度融合具有一定的参考意义。

2021, 36(2): 16-27.

摘要:

构建多渠道机制下数字经济影响出口贸易的理论模型,利用2008—2017年中国省级面板数据,实证检验数字经济对制造业高质量走出去的空间溢出效应、非线性边际递增效应及影响机制。研究结果表明:数字经济显著促进了中国省级出口技术复杂度的提升,其产生的正向空间溢出效应能助推出口贸易的高质量发展;数字经济的空间溢出效应存在区域异质性,沿海省份较内陆省份享受了更多的数字红利;数字经济对出口技术复杂度的影响具有动态非线性驱动效应,出口贸易水平较高的地区享受的数字经济红利更大;通过人力资本与贸易成本两个渠道,数字经济能间接提升省级出口技术复杂度;数字经济作用于实体经济时普遍存在边际递增的网络效应。因而应加强数字经济基础设施建设,优化创新环境,让数字经济的发展推动我国制造业高质量走出去。

构建多渠道机制下数字经济影响出口贸易的理论模型,利用2008—2017年中国省级面板数据,实证检验数字经济对制造业高质量走出去的空间溢出效应、非线性边际递增效应及影响机制。研究结果表明:数字经济显著促进了中国省级出口技术复杂度的提升,其产生的正向空间溢出效应能助推出口贸易的高质量发展;数字经济的空间溢出效应存在区域异质性,沿海省份较内陆省份享受了更多的数字红利;数字经济对出口技术复杂度的影响具有动态非线性驱动效应,出口贸易水平较高的地区享受的数字经济红利更大;通过人力资本与贸易成本两个渠道,数字经济能间接提升省级出口技术复杂度;数字经济作用于实体经济时普遍存在边际递增的网络效应。因而应加强数字经济基础设施建设,优化创新环境,让数字经济的发展推动我国制造业高质量走出去。

2019, 34(5): 4-21.

摘要:

以环保经历嵌入为研究视角, 基于2008—2016年中国沪深A股重污染企业的经验证据, 实证检验高管环保经历嵌入对企业绿色转型的影响及其机制。研究发现:环保经历嵌入能有效促进企业绿色转型; 环保经历嵌入管理层和董事会均能显著地提高企业绿色转型水平, 但环保经历嵌入监事会的影响不显著。进一步研究发现, 新《环境保护法》实施后, 环保经历嵌入对企业绿色转型的促进作用更加显著, 并主要表现在民营企业与低融资约束企业中, 其作用路径一般是通过提高企业创新水平和降低企业调整成本来促进企业绿色转型。因此, 为推进企业绿色转型, 聘请和重视环保经历人才有助于降低绿色转型的风险和成本。

以环保经历嵌入为研究视角, 基于2008—2016年中国沪深A股重污染企业的经验证据, 实证检验高管环保经历嵌入对企业绿色转型的影响及其机制。研究发现:环保经历嵌入能有效促进企业绿色转型; 环保经历嵌入管理层和董事会均能显著地提高企业绿色转型水平, 但环保经历嵌入监事会的影响不显著。进一步研究发现, 新《环境保护法》实施后, 环保经历嵌入对企业绿色转型的促进作用更加显著, 并主要表现在民营企业与低融资约束企业中, 其作用路径一般是通过提高企业创新水平和降低企业调整成本来促进企业绿色转型。因此, 为推进企业绿色转型, 聘请和重视环保经历人才有助于降低绿色转型的风险和成本。

2022, 37(1): 58-74.

摘要:

建设数字中国与实现绿水青山都是推动新时代经济高质量发展的重要战略举措。利用2005—2019年中国283个城市的面板数据,在环境库兹涅茨曲线理论的框架下,基于国家级大数据综合试验区这一准自然实验,运用多期DID和PSM-DID方法,评估以数据要素为核心的数字经济发展对城市空气质量的影响。研究结果表明:数字经济发展对城市空气质量的改善作用显著,且减排效应呈厚积薄发的特征;异质性研究表明,数字经济对秦岭—淮河一线以北的城市空气质量具有更强的影响效应,且在较大规模、高互联网发展水平以及低财政支出水平的城市其减排效应更加明显;机制检验表明,数字经济通过推动产业升级、促进技术创新以及优化资源配置改善了城市空气质量;进一步研究表明,数字经济的发展不仅推动了本地空气质量的改善,而且对降低相邻城市的空气污染也具有激励作用。因此,要进一步推动大数据试验区建设,提升该政策战略执行的包容性和灵活度,同时完善信息基础设施建设,以充分发挥数字经济对城市空气质量的改善作用。

建设数字中国与实现绿水青山都是推动新时代经济高质量发展的重要战略举措。利用2005—2019年中国283个城市的面板数据,在环境库兹涅茨曲线理论的框架下,基于国家级大数据综合试验区这一准自然实验,运用多期DID和PSM-DID方法,评估以数据要素为核心的数字经济发展对城市空气质量的影响。研究结果表明:数字经济发展对城市空气质量的改善作用显著,且减排效应呈厚积薄发的特征;异质性研究表明,数字经济对秦岭—淮河一线以北的城市空气质量具有更强的影响效应,且在较大规模、高互联网发展水平以及低财政支出水平的城市其减排效应更加明显;机制检验表明,数字经济通过推动产业升级、促进技术创新以及优化资源配置改善了城市空气质量;进一步研究表明,数字经济的发展不仅推动了本地空气质量的改善,而且对降低相邻城市的空气污染也具有激励作用。因此,要进一步推动大数据试验区建设,提升该政策战略执行的包容性和灵活度,同时完善信息基础设施建设,以充分发挥数字经济对城市空气质量的改善作用。

2022, 37(3): 4-20.

摘要:

数字经济是促进新时代经济高质量增长的重要引擎。基于2011—2019年30个省份的面板数据,分别利用熵值法和DEA-Malmquist指数法测算我国省级数字经济发展综合指数与全要素生产率,实证探讨数字经济对经济高质量发展的影响效应。研究发现:数字经济能显著促进经济高质量发展,该结论经过一系列稳健性检验后仍显著成立;机制分析表明,数字经济是通过提升区域创新水平、加快产业结构升级赋能于经济高质量发展;进一步分析表明,数字经济对相邻地区的经济高质量发展存在空间溢出效应,数字经济对经济高质量发展的促进效应因区域、生产率与人力资本的不同而存在异质性。因而应积极推进数字化基础设施建设,协调好各地区数字经济的均衡发展,实施数字化驱动发展战略,推进经济的高质量发展。

数字经济是促进新时代经济高质量增长的重要引擎。基于2011—2019年30个省份的面板数据,分别利用熵值法和DEA-Malmquist指数法测算我国省级数字经济发展综合指数与全要素生产率,实证探讨数字经济对经济高质量发展的影响效应。研究发现:数字经济能显著促进经济高质量发展,该结论经过一系列稳健性检验后仍显著成立;机制分析表明,数字经济是通过提升区域创新水平、加快产业结构升级赋能于经济高质量发展;进一步分析表明,数字经济对相邻地区的经济高质量发展存在空间溢出效应,数字经济对经济高质量发展的促进效应因区域、生产率与人力资本的不同而存在异质性。因而应积极推进数字化基础设施建设,协调好各地区数字经济的均衡发展,实施数字化驱动发展战略,推进经济的高质量发展。

2022, 37(2): 71-87.

摘要:

“双循环”背景下,新型城镇化不仅是经济发展的新动力,也是实现共同富裕的有力支撑。基于扎实推进共同富裕的背景,从富裕水平、区域差距和城乡差距三方面构建共同富裕的指标体系,测算了281个城市的共同富裕水平,并采用SARAR模型分析新型城镇化对共同富裕的影响。研究发现:推进地区经济发展是实现共同富裕的根本途径;新型城镇化和共同富裕存在着空间相关性,且新型城镇化对共同富裕及其各维度产生显著的促进作用;共同富裕不仅受新型城镇化的影响,还受到城市初始经济发展的影响;比较而言,新型城镇化更能够提升贫困地区的共同富裕水平;新型城镇化对共同富裕产生直接作用的同时,还会通过农民收入和公共服务对共同富裕产生间接的促进作用。在推进新型城镇化过程中,可从提高富裕水平、缩小城乡收入差距和区域经济差距角度助推共同富裕。

“双循环”背景下,新型城镇化不仅是经济发展的新动力,也是实现共同富裕的有力支撑。基于扎实推进共同富裕的背景,从富裕水平、区域差距和城乡差距三方面构建共同富裕的指标体系,测算了281个城市的共同富裕水平,并采用SARAR模型分析新型城镇化对共同富裕的影响。研究发现:推进地区经济发展是实现共同富裕的根本途径;新型城镇化和共同富裕存在着空间相关性,且新型城镇化对共同富裕及其各维度产生显著的促进作用;共同富裕不仅受新型城镇化的影响,还受到城市初始经济发展的影响;比较而言,新型城镇化更能够提升贫困地区的共同富裕水平;新型城镇化对共同富裕产生直接作用的同时,还会通过农民收入和公共服务对共同富裕产生间接的促进作用。在推进新型城镇化过程中,可从提高富裕水平、缩小城乡收入差距和区域经济差距角度助推共同富裕。

2020, 35(2): 55-67.

摘要:

以2008—2017年我国A股上市公司为研究样本, 实证检验了资产剥离对企业财务绩效的影响及其作用机制。研究发现, 资产剥离的实施能够显著影响企业的财务绩效, 其对企业财务绩效的作用方向取决于剥离前企业的业绩基础, 即对于经营不佳的企业而言, 资产剥离损害了企业财务绩效, 反之则显著提升了企业财务绩效。机制检验表明, 融资约束在资产剥离与企业财务绩效的负向关系中发挥了中介效应, 投资效率在资产剥离与企业财务绩效的正向关系中发挥了中介效应。

以2008—2017年我国A股上市公司为研究样本, 实证检验了资产剥离对企业财务绩效的影响及其作用机制。研究发现, 资产剥离的实施能够显著影响企业的财务绩效, 其对企业财务绩效的作用方向取决于剥离前企业的业绩基础, 即对于经营不佳的企业而言, 资产剥离损害了企业财务绩效, 反之则显著提升了企业财务绩效。机制检验表明, 融资约束在资产剥离与企业财务绩效的负向关系中发挥了中介效应, 投资效率在资产剥离与企业财务绩效的正向关系中发挥了中介效应。

2021, 36(1): 98-112.

摘要:

员工持股计划作为企业内部的一项集体激励政策,在优化企业产权配置的同时亦对企业融资能力产生重要影响。基于2011—2018年A股上市公司样本,探究员工持股计划对企业融资约束的影响及作用机制,研究发现,员工持股计划通过降低外部融资成本来缓解企业的融资约束状况,这种缓解作用对东部地区的企业以及民营企业更为显著;员工持股计划通过增强员工身份认同、缓解员工层面代理问题等途径来提升企业内部控制质量,内部控制质量在员工持股计划与融资约束作用之间起到部分中介作用;由于员工之间的“监督效应”及员工持股计划的“公告效应”,员工持股计划在提升内部控制质量方面不存在“搭便车”行为,在缓解融资约束方面存在“1/N”效应。本研究结论为新时期推进员工持股深化改革、提升本土企业内部竞争力提供了参考。

员工持股计划作为企业内部的一项集体激励政策,在优化企业产权配置的同时亦对企业融资能力产生重要影响。基于2011—2018年A股上市公司样本,探究员工持股计划对企业融资约束的影响及作用机制,研究发现,员工持股计划通过降低外部融资成本来缓解企业的融资约束状况,这种缓解作用对东部地区的企业以及民营企业更为显著;员工持股计划通过增强员工身份认同、缓解员工层面代理问题等途径来提升企业内部控制质量,内部控制质量在员工持股计划与融资约束作用之间起到部分中介作用;由于员工之间的“监督效应”及员工持股计划的“公告效应”,员工持股计划在提升内部控制质量方面不存在“搭便车”行为,在缓解融资约束方面存在“1/N”效应。本研究结论为新时期推进员工持股深化改革、提升本土企业内部竞争力提供了参考。

2021, 36(2): 69-85.

摘要:

相较于美国式面向全体员工的退休储蓄型计划,中国式员工持股计划面向关键少数员工,员工大多自行出资,持股期更加灵活。基于2011—2017年A股上市公司数据,研究员工持股计划与企业创新产出数量与质量之间的关系;并进一步依据员工持股计划的契约特征将其分为治理型、激励型与绑定型三类,研究不同路径取向下的员工持股计划对企业创新的影响差异。结果表明:相对于治理型计划,激励型计划与绑定型计划均能提升企业的创新产出,且绑定型计划的作用更加显著;影响机制检验发现,激励型计划促进了员工在创新活动中的努力投入,绑定型计划降低了员工流失率并提升了高管的风险承担水平。本研究证实员工持股计划的实施符合利益协同观而非市值管理观,中国式员工持股计划具有创新促进效应。

相较于美国式面向全体员工的退休储蓄型计划,中国式员工持股计划面向关键少数员工,员工大多自行出资,持股期更加灵活。基于2011—2017年A股上市公司数据,研究员工持股计划与企业创新产出数量与质量之间的关系;并进一步依据员工持股计划的契约特征将其分为治理型、激励型与绑定型三类,研究不同路径取向下的员工持股计划对企业创新的影响差异。结果表明:相对于治理型计划,激励型计划与绑定型计划均能提升企业的创新产出,且绑定型计划的作用更加显著;影响机制检验发现,激励型计划促进了员工在创新活动中的努力投入,绑定型计划降低了员工流失率并提升了高管的风险承担水平。本研究证实员工持股计划的实施符合利益协同观而非市值管理观,中国式员工持股计划具有创新促进效应。

Periodical Information

Bimonthly,Founded in 1986

Supervisor:Education Department of Guangdong Province

Sponsor:Guangdong University of Finance and Economics

Editor:Editorial Office of Journal of Guangdong University of Finance and Economics

Publisher:Periodical Center of Guangdong University of Finance and Economics

Editor-in-Chief:Zhang Kai

Director:Peng Rong

Address:

21 Luntou Road, Guangzhou

Tel:020-84096712、84096029

Email:

Standard serial number:

ISSN 1008-2506

CN 44-1711/F

Post Code:46-295

Domestic Sales:Guangdong Provincial Bureau of Newspapers and Periodicals

Distribution:Public offering at home and abroad

Price:10 yuan/period,The year 60 yuan

Journal Of Retrieval

Advanced Search

Journal Of Retrieval

Classification Retrieval

Links

More